Research and Background

Research and Background

The research foundation for this strategy comes from three main strands of literature: skewness-based return prediction, online change-point detection, and short-horizon technical signal conditioning. The first strand is especially relevant because the strategy begins by ranking stocks using a skewness-based measure derived from intraday returns. In asset pricing and empirical market microstructure, skewness is not treated as just a descriptive statistic; it is often studied as a feature that captures asymmetry in return distributions and helps distinguish lottery-like price behavior from more balanced distributions. In one of the most relevant papers for this approach, Amaya, Christoffersen, Jacobs, and Vasquez (2015), “Does Realized Skewness Predict the Cross-Section of Equity Returns?”, the authors show that realized skewness computed from high-frequency returns has predictive power for future stock returns. Their headline result is economically intuitive for signal construction: stocks with relatively low realized skewness outperform stocks with relatively high realized skewness in the following period. That finding is closely aligned with cross-sectional strategies that sort securities by skewness and then treat the tails of the distribution differently.

A related line of work helps explain why skewness can be informative in the first place. Chen, Hong, and Stein (2001), “Forecasting Crashes: Trading Volume, Past Returns, and Conditional Skewness in Stock Prices,” argues that skewness is linked to the way information diffuses through markets and to the buildup of one-sided investor expectations. Their results show that return asymmetry is not random noise; it co-moves with market conditions and investor behavior, especially in names that have recently experienced strong moves and unusual trading activity. More recent work such as Amaya et al. (2012), “Realized Skewness,” formalizes how skewness can be measured from high-frequency data and shows that the third moment of returns is economically meaningful rather than incidental. Taken together, this literature supports the idea that skewness-based signals can help identify stocks whose recent return distributions are unusually imbalanced, and therefore potentially more attractive for cross-sectional selection.

The second major research pillar is Bayesian Online Change-Point Detection, which is used in this strategy as the real-time trigger after the cross-sectional skewness ranking is complete. The foundational reference here is Adams and MacKay (2007), “Bayesian Online Changepoint Detection.” Their framework provides a recursive Bayesian method for identifying abrupt changes in the underlying generating process of a time series as new observations arrive. Instead of requiring a full sample and looking backward, BOCPD is explicitly designed for online decision-making: it updates the posterior probability of a new regime at each step and tracks how likely it is that the current sequence has shifted. That makes it especially attractive in intraday trading, where the goal is not merely to classify a stock once per day, but to detect whether a fresh intraday move is beginning to develop in real time. More recent extensions of the BOCPD framework continue to emphasize its usefulness for sequential inference in evolving time series, particularly when structural shifts matter for prediction.

The final strand of literature relates to the use of technical state filters before acting on a signal. This strategy uses a momentum-state filter based on changes in RSI before proceeding to the skewness classification step. While the exact implementation is strategy-specific, the general research backdrop comes from the literature on technical trading rules and short-horizon signal extraction. A classic reference is Brock, Lakonishok, and LeBaron (1992), “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns,” which shows that simple rule-based indicators can contain information about future return behavior that is not obviously explained by random walk benchmarks. The relevance here is not that RSI itself is a magic predictor, but that technical filters can be used as a first-stage conditioning mechanism to isolate a subset of securities where the subsequent signal may be more informative. In combination, these three strands of research suggest a coherent framework: use skewness to locate asymmetric cross-sectional opportunities, use an online change-point model to wait for intraday confirmation, and use a technical state filter to avoid acting on a completely unconditioned universe.

Strategy Construction

Strategy Construction

The strategy is designed as a multi-stage intraday reversal framework that combines cross-sectional selection with real-time signal confirmation. It begins with a broad universe of liquid Indian equities, filtered for tradeability and minimum market capitalization so that the resulting opportunity set is both sufficiently large and practically executable. From this universe, the strategy does not immediately trade every stock. Instead, it first applies a technical conditioning step to identify names that are showing a sufficiently large recent change in short-term momentum state. This acts as a screening layer that narrows the universe before any more computationally intensive ranking or intraday monitoring takes place.

After this first filter, the strategy computes a skewness-based measure from recent intraday returns and uses that to rank the remaining stocks cross-sectionally. The basic idea is to identify names whose recent return distributions are unusually asymmetric relative to the rest of the universe. Rather than treating all stocks the same, the framework focuses on the tails of the skewness distribution, because those names are more likely to reflect one-sided positioning, unstable short-term sentiment, or return distributions that may be prone to reversal or continuation depending on the intraday regime. At this stage, the strategy identifies a long basket and a short basket from opposite ends of the skewness ranking, but it still does not enter immediately.

The actual trade entry is delayed until the strategy receives intraday confirmation from a Bayesian Online Change-Point Detection model running on completed 5-minute bars. This is a key architectural feature: the cross-sectional skewness signal decides where to look, while the BOCPD model decides when to act. In practice, the strategy waits for evidence that the intraday return process has shifted sufficiently in the direction consistent with the desired trade. This avoids entering purely on a daily ranking signal and instead requires the market to reveal a fresh intraday move before capital is committed.

Risk management is then handled as a separate real-time layer. Profit thresholds and stop thresholds are estimated from recent return behavior and updated at the instrument level, so risk is not imposed uniformly across all names. The strategy also monitors momentum divergence between the recent price path and the BOCPD state, allowing positions to be exited not only on conventional profit-taking or stop-loss rules, but also when the live intraday behavior begins to contradict the original signal. Finally, all positions are closed before the end of the trading session, keeping the framework strictly intraday and ensuring that the strategy is exposed only to the price discovery process unfolding during market hours rather than to overnight event risk.

Live Performance

Live Performance

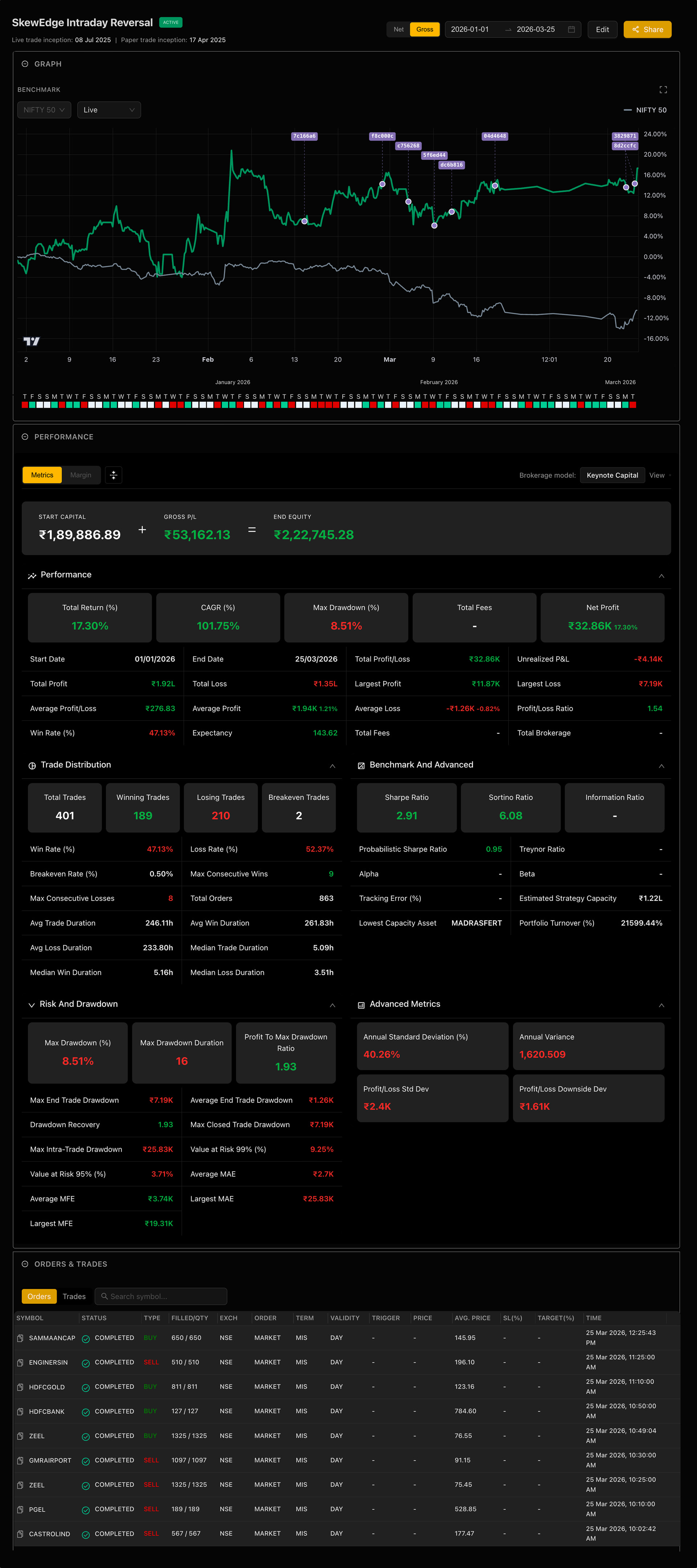

Since the beginning of 2026, the strategy has been deployed in a live or paper-trading environment, providing a forward-looking validation of the underlying framework. Over this period, the equity curve has shown a steady upward trajectory, with relatively controlled drawdowns and consistent recovery phases.

The current live performance snapshot shows the strategy delivering strong results against the NIFTY 50 benchmark. In the period displayed on the dashboard, from 1 January 2026 to 25 March 2026, the strategy is up by roughly 12–14% on a gross basis, while the NIFTY 50 is down around 11–12% over the same period.

What stands out is not just the positive return, but the relative strength. The strategy has continued to advance in a period where the broader market has been weak, highlighting the robustness of the intraday reversal framework and its ability to capture opportunities that are less dependent on overall market direction.

The live curve also reflects real trading conditions rather than a smooth hypothetical path. There are periods of pause and short drawdowns, followed by recovery and progression, which is consistent with how a genuine intraday systematic strategy behaves in production.

This live performance adds important weight to the research behind the strategy. It shows that the combination of skewness-based stock selection, intraday reversal signals, and systematic execution discipline is translating effectively from model design into live results.

Closing Thought

Closing Thought

Markets often reveal their inefficiencies in moments of imbalance—when positioning becomes one-sided and short-term behavior turns unstable. The SkewEdge Intraday Reversal strategy is built around systematically identifying and acting on those moments, combining cross-sectional signals with real-time confirmation rather than relying on static assumptions.

What makes the framework meaningful is not just the research foundation, but its ability to operate under live market conditions. As with any systematic approach, its strength lies in consistency of execution and disciplined risk management over time, rather than any single period of performance.

References

References

For a complete breakdown of the SkewEdge Intraday Reversal Strategy, including the logic, market conditions, and how it is executed systematically, refer to the materials below.

Our materials -

Watch the full YouTube video for a detailed breakdown of the SkewEdge Intraday Reversal Strategy here: SkewEdge Intraday Reversal Strategy

![]() Strategy Document (PDF)

Strategy Document (PDF)

Clear write-up of the SkewEdge Intraday Reversal strategy explaining the hypothesis, RDSKEW-based stock selection, BOCPD-driven entry logic, exit rules, and risk framework.

Link: View Here

Research Paper Pack (Folder)

Research Paper Pack (Folder)

Selected research on return skewness, intraday reversals, and regime shift detection that supports the logic behind skew-based mean reversion strategies.

Link: View Here

Contact us

Contact us

If you’d like the full research pack, detailed backtest outputs, or a walkthrough of how we implement the SkewEdge Intraday Reversal Strategy systematically on Wizzer, reach us on WhatsApp: +91-8928065586