Research and Background

Earnings quality, accruals, and why cash matters

A large body of academic research has shown that not all earnings are equal. Two companies may report similar profits, but the quality of those earnings can differ significantly depending on how much is supported by actual cash flows.

One of the most influential findings in this space is the accrual anomaly, introduced by Sloan (1996). The core idea is simple:

companies with high accruals (earnings driven more by accounting adjustments than cash) tend to underperform, while companies with low or negative accruals tend to outperform over time.

The intuition is that cash-based earnings are more persistent, while accrual-based earnings are more likely to reverse.

This is reinforced by later work such as Richardson et al. (2005), which shows that different components of earnings have different reliability — with accrual-heavy earnings being less durable and more prone to correction.

Why markets misprice earnings quality

If this relationship exists, why does it persist?

One explanation is investor focus on headline earnings. Markets often anchor on reported profit numbers without fully adjusting for how those profits are generated. This leads to:

-

Overvaluation of firms with “inflated” accounting earnings

-

Undervaluation of firms generating strong operating cash flows

There is also a behavioral component. Investors tend to extrapolate recent performance, assuming that high reported earnings will continue, even when those earnings are not supported by cash generation.

This creates a systematic opportunity:

identify companies where cash flows are stronger than accounting profits, and where earnings quality is likely being underappreciated.

Combining fundamentals with risk control

While fundamental signals like accruals are powerful, they operate over longer horizons and can be exposed to market volatility.

This is why many systematic strategies combine:

-

Fundamental selection (what to buy)

-

Rule-based risk management (when to exit)

Volatility-adjusted approaches such as ATR-based exits are widely used to manage downside risk dynamically, allowing positions to adapt to changing market conditions while avoiding rigid stop levels.

Putting it together

The takeaway from the literature is clear:

-

Earnings backed by cash flow are more reliable

-

Accrual-heavy earnings are less persistent

-

Markets do not always price this distinction correctly

This strategy builds directly on that idea by systematically selecting high-quality large-cap companies, and managing them with a disciplined, rule-based framework.

Strategy Construction

The strategy is a long-only, systematic portfolio of NSE large-cap stocks, combining fundamental screening with disciplined execution and risk control.

Each month, the strategy evaluates a large-cap universe and selects companies that meet strict earnings quality criteria — specifically, firms where operating cash flow is strong, profits are positive, and cash generation exceeds reported earnings. From this filtered set, stocks are ranked based on an accrual-based measure, with preference given to companies showing lower or negative accruals, indicating higher-quality earnings.

Instead of fully rebuilding the portfolio every month, the strategy follows a slot-based approach. It maintains a target number of holdings and only adds new positions when existing ones exit. This allows winners to continue compounding while gradually introducing new opportunities, reducing unnecessary turnover.

Risk management is handled through a volatility-aware exit framework. Positions are monitored daily using ATR-based thresholds that adapt to each stock’s price behavior. This ensures that downside risk is controlled while still allowing trends to play out. All decisions — entries, exits, and capital deployment — follow a fully rules-based process, ensuring consistency and repeatability.

Backtests

All backtests are implemented on Wizzer, with a focus on realistic execution and production-ready assumptions.

We explicitly enforce:

-

Point-in-time universe construction (no survivorship bias)

-

Corporate-action adjusted data

-

Rule-consistent monthly execution

-

Daily monitoring for exits

-

Realistic transaction cost assumptions via Castlegate Capital

Evaluation focuses not just on returns, but also on drawdowns, turnover, and portfolio stability, ensuring the strategy is implementable in real-world conditions.

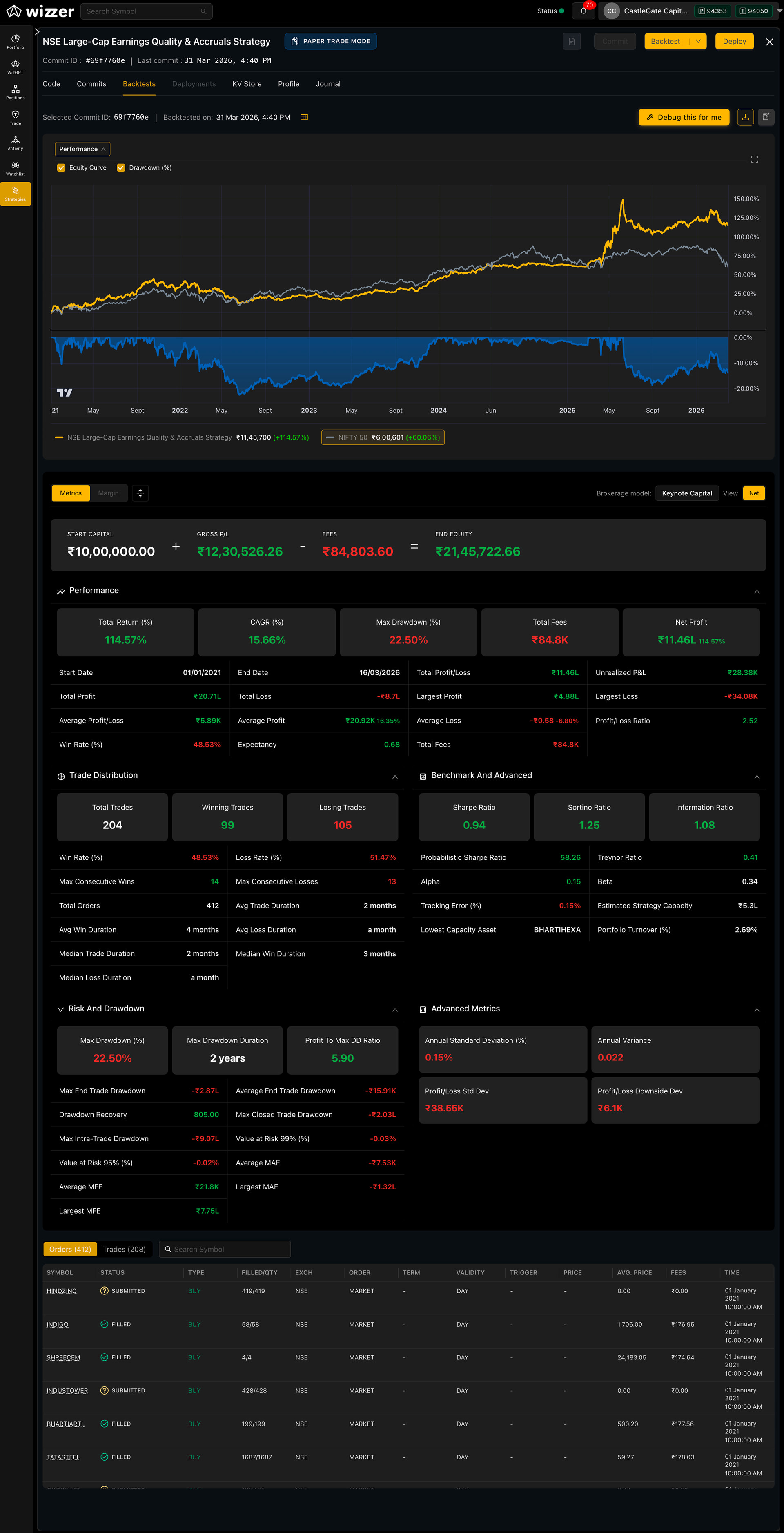

Outcomes

This backtest (01 Jan 2021 to 16 Mar 2026) shows a strong quality-driven compounding profile.

-

Total Return: +114.57%

-

CAGR: ~15.66%

-

Max Drawdown: ~22.50%

-

Net Profit: ₹11.46L on ₹10L capital

A few things stand out:

-

The strategy delivers steady long-term growth, driven by holding high-quality companies rather than frequent trading

-

Drawdowns are controlled relative to the return profile, with a strong profit-to-drawdown ratio (~5.9)

-

The portfolio maintains low turnover and disciplined capital deployment, consistent with its design

In terms of trade characteristics:

-

204 total trades over ~5 years

-

~48.5% win rate with a strong profit/loss ratio (~2.5)

-

Long holding periods, allowing compounding to work

Overall, the results support the core thesis:

a systematic focus on earnings quality and low accruals, combined with disciplined risk management, can generate meaningful long-term outperformance in large-cap equities.

Our materials -

![]() Strategy Document (PDF)

Strategy Document (PDF)

Clear write-up of the NSE Large-Cap Earnings Quality & Accruals Strategy explaining the hypothesis, RDSKEW-based stock selection, BOCPD-driven entry logic, exit rules, and risk framework.

Link: NSE Large-Cap Earnings Quality & Accruals Strategy

Contact us

If you’d like the full research pack, detailed backtest outputs, or a walkthrough of how we build and deploy systematic strategies on Wizzer with Castlegate Capital execution, WhatsApp us:

![]() +91-8928065586

+91-8928065586