Research and Background

Overnight price gaps are a well‑documented phenomenon in equity markets. A price gap occurs when the opening price of a security differs materially from the previous session’s closing price. These discontinuities typically arise because information arrives when markets are closed. Earnings announcements, macroeconomic developments, analyst revisions, and global market movements are incorporated into prices at the next market open through the opening auction. As a result, the opening print often represents a discrete adjustment to reflect newly available information.

A number of empirical studies have documented that overnight and intraday returns behave very differently. For example, French (1980) showed that a substantial portion of equity returns occurs outside regular trading hours. Later work by Stoll and Whaley (1990) examined the mechanics of the opening process and demonstrated that the opening price can be strongly influenced by accumulated order imbalances from overnight trading intentions. These findings highlight that the opening auction is a unique market environment where prices adjust rapidly and liquidity can be temporarily limited.

Research has also found that large overnight price movements can be followed by intraday reversals. A widely cited study by Cooper, Cliff, and Gulen (2008) examines overnight returns and shows that extreme overnight price changes often partially reverse during the trading day. The authors argue that large overnight moves may reflect temporary imbalances or overreaction to information rather than a fully efficient incorporation of news. This evidence provides empirical support for trading strategies that respond to unusually large opening price moves.

Market microstructure research further explains why such reversals may occur. Chordia, Roll, and Subrahmanyam (2002) show that liquidity provision and order‑flow imbalances can generate short‑term return reversals as markets absorb temporary demand shocks. When large buy or sell imbalances are present at the open, liquidity providers may initially accommodate the order flow, after which prices gradually revert as inventories are rebalanced during continuous trading.

Behavioral finance also offers an explanation for extreme price adjustments. Models such as Daniel, Hirshleifer, and Subrahmanyam (1998) suggest that investors can overreact to new information due to overconfidence and biased belief updating. When news arrives overnight, traders may push prices beyond fundamental value at the open, particularly in less liquid securities. As more participants enter the market during the session, prices may move back toward equilibrium.

Taken together, these strands of literature highlight several empirical patterns relevant to gap trading. First, overnight information frequently leads to discrete price adjustments at the open. Second, the opening auction can amplify price moves because liquidity is temporarily limited and order imbalances accumulate overnight. Third, extreme price adjustments may partially reverse intraday as liquidity providers, arbitrageurs, and additional market participants interact during continuous trading. These empirical findings form the foundation for systematic strategies that study and exploit the statistical behavior of large overnight gaps.

Strategy Construction

The strategy is built as a systematic intraday framework that focuses on exploiting abnormal overnight gap‑ups in equities. The core idea is that when a stock opens significantly higher than its previous close, the move can sometimes represent a temporary price dislocation caused by overnight news, liquidity imbalances, or opening auction dynamics. The framework scans a broad universe of equities each morning and identifies stocks that have experienced unusually large positive gaps relative to their recent historical behavior. These gap‑up events form the basis for potential short positions, with the expectation that some of these extreme moves partially revert during the intraday trading session.

The strategy operates on a diversified universe of mid‑ and small‑capitalization stocks. Using a broad cross‑section of stocks increases the number of observable gap events each day and allows the strategy to diversify across many independent signals rather than relying on a small number of instruments. After the market opens and the initial auction volatility settles, the system evaluates these gap events and selectively enters short positions in stocks exhibiting unusually large upward dislocations.

Risk management is embedded directly into the framework through adaptive position controls and strict intraday exposure rules. Capital is distributed across multiple qualifying trades to avoid concentration risk, and each position is monitored using dynamic stop mechanisms that adjust according to the magnitude of the initial gap. As trades move in the favorable direction, stops tighten to protect profits while preventing risk from expanding. Additionally, the strategy maintains a purely intraday holding period, closing all positions before the end of the session to eliminate overnight exposure and isolate the intraday behavior of gap events.

Backtests

All backtests are implemented on Wizzer, mirroring live constraints as closely as possible.

We specifically ensure:

Point‑in‑time universe / membership: the strategy is tested on what was actually investable at each date (no survivorship shortcuts).

Corporate‑action adjusted series: prices reflect splits/bonuses/dividends where applicable.

Realistic execution assumptions: fees and transaction costs are included so results are not “paper perfect.”

Backtest logic mirrors the live workflow: signal formation, position caps, order timing, and exits follow the same rule structure used in deployment.

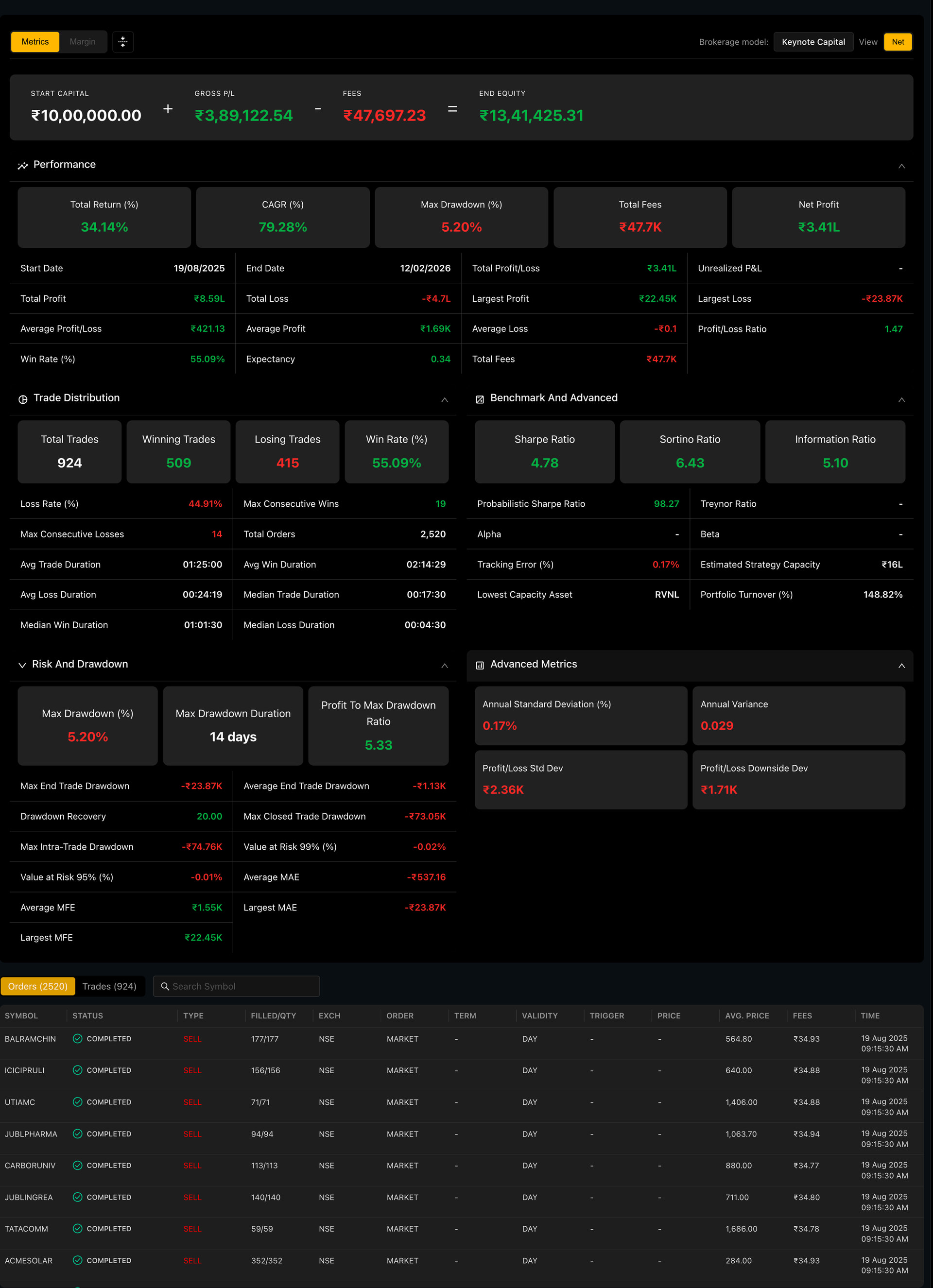

Outcomes

The backtest results are strong both in absolute and risk-adjusted terms. Over the test period, the strategy generated a 34.14% total return, growing capital from ₹10.0 lakh to ₹13.41 lakh. On an annualized basis, this corresponds to a 79.28% CAGR, which is notable for a purely intraday strategy.

Just as importantly, the return profile remained well controlled. The strategy recorded a maximum drawdown of only 5.20%, alongside a Sharpe ratio of 4.78 and a Sortino ratio of 6.43. Trade-level performance was also solid, with 924 trades and a 55.09% win rate. Taken together, these results suggest that the strategy was not only profitable, but also delivered returns with a relatively favorable risk profile.

References

For a complete breakdown of the Intraday Short Reversal Strategy, including the logic, market conditions, and how it is executed systematically, watch the full video here: Intraday Short Reversal Strategy

Our materials -

Strategy Document (PDF)

Clear write-up of the Intraday Short Reversal strategy explaining the hypothesis, entry/exit rules, key filters, and risk management framework used to capture reversals after strong gap-up openings.

Research Paper Pack (Folder)

Selected research on overnight gaps, short-term reversals, and intraday price behavior that supports the logic behind gap-based mean reversion strategies.

Contact us

If you’d like the full research pack, detailed backtest outputs, or a walkthrough of how we implement the Intraday Short Reversal Strategy systematically on Wizzer, reach us on WhatsApp: +91-8928065586