1. Research and Background

The research foundation for this strategy comes from three closely related strands of literature: change-point detection in time series, trend and momentum conditioning, and short-horizon reversal or mean-reversion behavior after strong short-term moves. The central methodological pillar is Bayesian Online Change-Point Detection, introduced by Adams and MacKay (2007). Their framework is designed for sequential decision-making in non-stationary time series, where the goal is to infer, as each new observation arrives, whether the underlying data-generating process has shifted. Rather than waiting for a full sample and then identifying regimes retrospectively, BOCPD updates the posterior probability of a new regime in real time. This is particularly relevant in intraday trading, where market conditions can change abruptly and signals must be evaluated as fresh data arrives rather than after the fact.

A second important strand comes from the literature on technical trading rules and trend-following state filters. A classic paper here is Brock, Lakonishok, and LeBaron (1992), which shows that simple technical rules can carry statistically meaningful information about future return behavior. More broadly, the trend-following literature, including Moskowitz, Ooi, and Pedersen (2012), documents that past price direction can contain predictive information across many asset classes and horizons. While this strategy is not a pure trend-following system, it clearly draws on the same intuition: before taking any short trade, it first filters for stocks already exhibiting persistent downside structure through measures such as downtrend state, candle behavior, and trading activity. In other words, it does not short strength in a random cross-section of stocks; it shortlists names that are already embedded in a broader bearish regime.

The third research strand concerns short-horizon reversals after strong recent moves, especially when returns exhibit temporary overshooting. Jegadeesh (1990) is one of the classic references showing that security returns can display predictable short-run reversal patterns. That literature is relevant here because the strategy first identifies stocks with a weak broader state, and then looks for names that are temporarily showing strong positive intraday drift. The setup is economically intuitive: a stock can be in an overall bearish structure while still experiencing a short-lived intraday burst upward, and such bursts may create attractive fade opportunities if they are interpreted as temporary rather than durable regime shifts. Taken together, these strands of research support a layered framework: use regime detection to identify unstable or shifting dynamics, use technical state filters to focus on structurally weak names, and then act when intraday behavior produces a short-term move that is favorable to fade.

2. Strategy Construction

The strategy is built as a multi-stage intraday short-selling framework that combines structural weakness, probabilistic regime detection, and tightly controlled execution. It begins with a broad universe of liquid Indian equities filtered for basic tradeability, including minimum market capitalization, minimum price, and minimum trading activity. From this universe, the strategy first applies a daily-level screening process. At this stage, it uses a Bayesian Online Change-Point Detection model on daily returns to identify stocks whose recent return path is consistent with continued downside drift and a relatively stable bearish regime. This creates an initial shortlist of names that are already weak from a broader directional perspective.

That shortlist is then refined using a second layer of filtering based on technical structure. The strategy checks whether the stock has exhibited persistent bearish behavior through features such as the balance of red candles over recent history, sufficient average trading volume, and a downtrend state from a Supertrend-style indicator. This step matters because it prevents the system from shorting temporary intraday strength in names that do not already have a broader bearish backdrop. Once those filters are satisfied, the strategy runs a second BOCPD screen on recent intraday returns and looks for stocks that are showing positive short-term drift. In effect, the strategy looks for stocks that are weak on the larger backdrop but temporarily strong intraday, creating a potential fade setup where strength is sold rather than followed.

Entries are placed during a defined morning window, with position size tied to a fixed fraction of portfolio value. Risk management is handled through several layers rather than a single stop rule. The strategy uses an initial hard stop derived from the stock’s recent average down-day behavior, then adds a state-dependent trailing mechanism that becomes stricter as profits build. In addition, the live intraday BOCPD state continues to be monitored after entry, so positions can be exited when the posterior change-point probability rises and the return process no longer supports the original short thesis. Finally, all positions are closed before the end of the session, keeping the strategy strictly intraday and isolating its performance to the market’s daytime price-discovery process rather than overnight event risk.

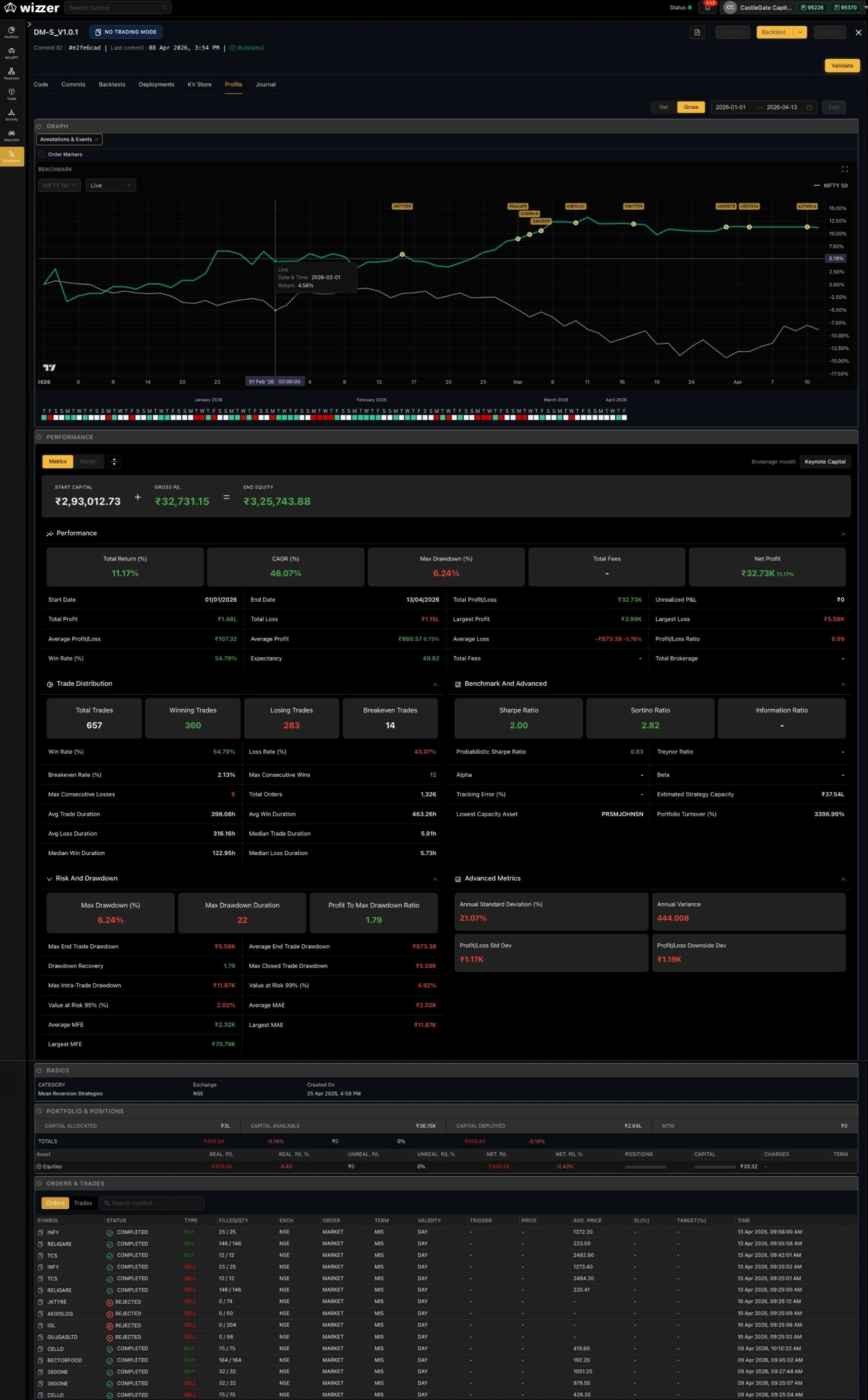

3. Live Performance Snapshot

References

References

For a complete breakdown of the DM-S (Drift Model – Short) strategy, including the signal logic, stock selection framework, and how persistent red-candle behaviour is translated into an intraday execution model, refer to the full strategy documentation and research materials below.

Our materials -

-

Strategy Document (PDF)

Clear write-up of the DM-S strategy outlining the core hypothesis of persistent selling pressure, stock selection logic based on red-candle behaviour, defined entry and exit rules, capital allocation methodology, and the intraday execution framework used to systematically capture downward drift. -

Watch the full YouTube video for a detailed breakdown of the DM-S_V1.0.1 Strategy here:

Contact us

Contact us

If you’d like the full research pack, detailed backtest outputs, or a walkthrough of how we implement the DM-S strategy systematically on Wizzer, reach us on WhatsApp: +91-8928065586